Centuryply is among India’s largest interior infrastructure product manufacturers. The Company offers plywood, laminates, veneers, MDF, blockboards, doors, fibre cement boards and particle boards. It is also engaged in the logistics business through the management of a container freight station (India’s first privately owned CFS at the Kolkata Port).

Another unit in Laos is being commissioned. 5000 retail outlets added in 2015-16.

Launched new age products– Zykron and Starke (Wood Polymer Composite and Cement Fibre Boards). CPL expects to carve a 10% market share of the country’s B1,000 cr fibre cement boards market by 2020

Set up a particle board unit at Chennai, commissioning in June 2016, to capitalise on the fact that there are no similar units in the city

Commenced the construction of MDF unit at Hoshiarpur (Punjab). Following the commissioning of this unit, prlanned for July 2017, CPL will possess a capacity to manufacture 198,000 cubic metres per annum, graduating it to one of the largest in the country.

Grew the laminates business by around 15% on the back of a strong catalogue and distribution network.

Plywood capacity continues at 210,000 cubic meters

Laminate capacity continues at 4.8 million sheets p.a. Conventionally, new laminates would be introduced every second year; Centuryply revolutionised the space with the introduction of four catalogues a year.

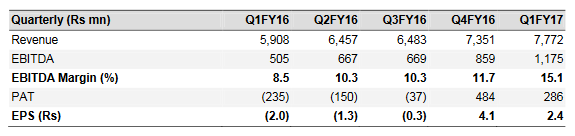

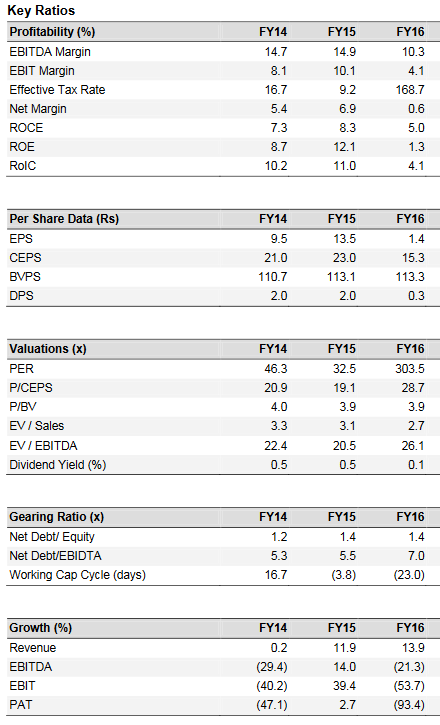

The co did not reduce prices even though the competition did amidst sluggish demand. CPL maintained EBIDTA margins at 17%.

Raw material costs as a proportion of revenues declined from 53% to 38% in the three years ending 2015-16.

Working capital cycle reduced from 88 days to 70 days.

Container Freight Station at the Kolkata Port contributed only 5% to revenues in 2015-16, the corresponding EBIDTA margin was 46%.

Industry structure and developments

Wood panel products - The Indian wood panel market is valued at 28,500 crore. Plywood has a share of 63% (18,000 crore).

Plywood - India’s plywood industry is likely to reach a market value of 479.7 billion by 2019. This growth in the plywood market is expected to be led by a surge in the growth of commercial and domestic developments.

The MDF market is estimated to be worth ~35 billion in India and has grown at a CAGR of ~5-8% over the last five years. The Central Government’s decision to withhold fresh licenses for the manufacture of plywood has widened the gap between demand and supply. This is a positive development for the MDF industry and will increase the use of engineered panel products.

Segment-wise performance

Plywood: Revenues from plywood business reported a growth of 2.94% from 1,243.06 crore in 2014-15 to 1,279.59 crore in 2015-16.

Laminates: Laminates reported a growth of 14.20% from 321.27 crore in 2014-15 to 366.89 crore in 2015-16.

Logistics: Revenues from the logistics sector reported a 12.50% growth from 75.42 crore in 2014-15 to 84.85 crore